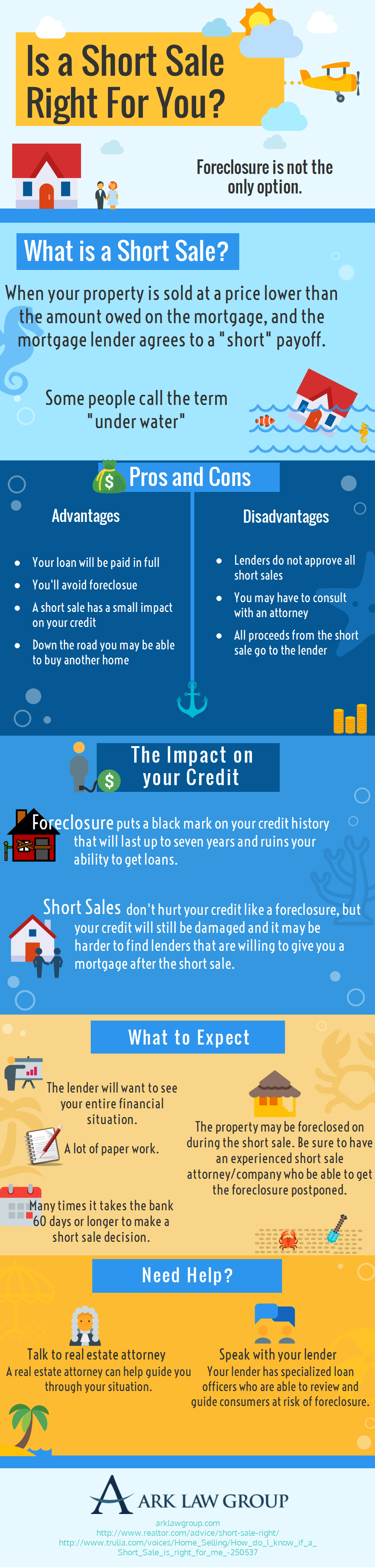

No one wants to lose their home to foreclosure because it’s a nightmare, everyone wants to avoid if possible. If your home has lost its value since the time you bought it and you owe more than it’s worth, you might want to consider a short sale. What short sale means is selling your house for less than the full amount you owe on your mortgage. A real estate agent will list your house at the price that’s close to the current value. When an offer is made on your home you present it to the bank/lender. A piece of cake, right? This is what can make the poses difficult — the lender or “lenders”, if you possess more than one loan on your home, must agree to the short sale terms of the sale. It could mean they forgive your debt, or they may not. It’s a financial decision only the lender can make. Here’s a quick overview of what you need to know about short sales, and whether or not it’s right for your situation and needs.

Is a Short Sale Right For You?

December 29, 2015

A dedicated full-time digital marketer with 12+ years of experience in the industry. Since 2015, he has been successfully running infographicportal.com, a platform that showcases high-quality infographics across various topics. Nagendra's expertise lies in creating and executing effective digital marketing strategies that drive engagement and growth. His passion for visual storytelling and commitment to excellence has made him a respected figure in the digital marketing community.

Thank you for the great infographic, it explained some the of basics of short sales very well. It’s important to consult with your bank, realtor, and attorney if you’re considering a short sale. It can be a great option but it’s something that can backfire if done incorrectly.